It was 7 pm on a Thursday night in February when one of the partners at my first firm out of college stopped by my cubicle holding a shoebox. “I’m going to need you to do the Johnson’s tax return, but first you’ll need to use these receipts to figure out their financials.” I was a staff tax accountant at the time, and this particular partner had a reputation for his short temper. I accepted my fate with a shrug and dug into it. “This partner should have retired years ago, so I guess he’s set in his ways,” I thought to myself, trying to excuse the incredible behavior.

It blew my mind that he let his client operate his business from a literal shoe box. How irresponsible to not take a proactive approach and teach his client the proper way to take care of his business. Cloud-based accounting systems existed at this time, and the client obviously had the money to pay for a decent accounting system.

What blew my mind further was when the young, cool partner dropped another shoe box at my desk two weeks later. This guy had no excuses and had at least twenty years left in his career. Was he really going to let his clients down by not having enough of a spine to teach them the proper way to handle their accounting? Or better yet, step up to be the accountant in the relationship rather than defaulting to letting his client figure out what to do with his accounting?

This is not going to be you. You are going to find an accountant to do your accounting for you so that you can focus on building your company. The first step in the process is graduating from managing your company with the bank account balance (the modern-day version of the shoe box) and managing your business with good finance and accounting systems.

Banking

On Tuesday, March 7, 2023, Silicon Valley Bank opened its doors as one of the most highly respected banks in the country. On Wednesday of that week, it announced that it needed to raise some capital to shore up its balance sheet. By Friday, the bank had collapsed and U.S. regulators took control of bank operations.

What could have proven truly tragic was mitigated in part when the FDIC promised to back depositors beyond the traditional $250,000 limit.

Scary as this event was, if a company is going to lose money from a banking crisis it likely won’t be from a run on the bank. More likely it will be for reasons completely in their control to prevent, but for some reason or another, choose not to take the needed measures to safeguard their cash.

The first step to safeguarding your cash is to select a reputable bank that has modernized systems that integrate well with your other systems. The bank should also have fraud prevention features that allow you to against check washing and other common schemes. Finally, the bank should also allow you to create user profiles with different access permissions related to the funds.

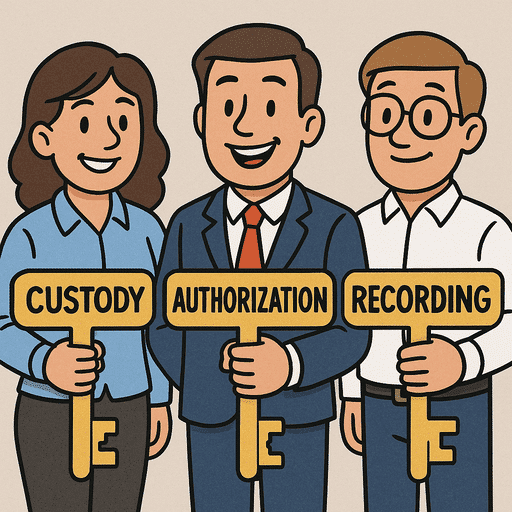

What bank permissions should you grant to team members? While it might be tempting to go with the most convenient route of giving full access to everyone who might eventually think they’ll need it, this policy is unwise if you want to keep your cash and prevent fraud. Specifically, three duties need to be segregated: custody, authorization, and recording. Elevated Tax & Accounting can help you set these controls correctly.

Custody

Custody involves physical possession or the ability to directly control physical or digital assets. The person who has custody should not be responsible for recording or authorizing related transactions. For example, an employee who handles cash receipts should not also be responsible for recording these receipts in the accounting records.

Authorization

Authorization is the approval of transactions and decisions. The person who authorizes transactions (like approving a vendor payment or authorizing a refund) should not have custody of related assets or be responsible for recording the transactions. This ensures that transactions are initiated for legitimate business purposes and reduces the risk of unauthorized activities.

Recording

Recording involves maintaining the organization’s books, recording transactions, and maintaining supporting documentation. The person responsible for recording transactions (like a bookkeeper or accountant) should not have custody of the assets involved in these transactions nor should they have permission to authorize transactions. This segregation helps to ensure that the records accurately reflect actual transactions and prevents any single person from both committing an irregularity and then concealing it in the records.

What If I Don’t Properly Segregate Duties?

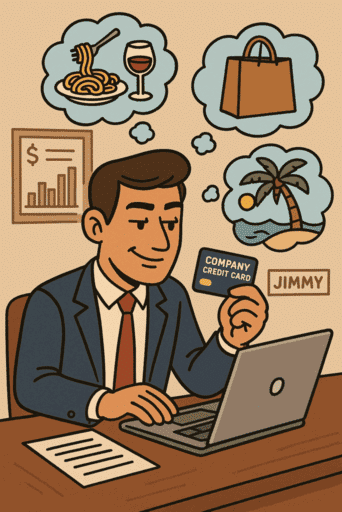

Let’s explore what can happen when duties are not properly segregated. First, let’s explore the most egregious violation of the segregation principle and imagine a scenario where a single employee, perhaps a co-founder named Jimmy, holds the keys to all three duties.

Jimmy has control over the company’s credit card (custody), the authority to approve expenses charged to the card (authorization) and is also responsible for recording these transactions in the company’s financial records (recording).

Jimmy works hard and justifies his use (custody) of the company credit card for personal expenses, such as dining out, shopping, or vacations, which are not related to business activities.

Because Jimmy has the authority to approve credit card transactions, he can easily validate these personal expenses as “business-related”.

In his role as the recorder of transactions, Jimmy can enter these personal expenses into the financial system to appear as legitimate business expenses, categorizing them in a way that makes them appear valid (e.g., labeling personal dining as client meetings).

Without anyone else reviewing the credit card statements or the financial records, these fraudulent activities could go undetected for a significant period. Jimmy’s co-founder might be baffled at why the company struggles financially and may never catch the fraud.

If you take away one of these keys, fraud becomes harder but not impossible. Let’s suppose you decide that founders should focus on building the business rather than doing the accounting and you hire an accounting firm to do that instead, thereby taking away Jimmy’s Recording key.

Suppose Jimmy is responsible for managing the petty cash (custody) and also has the authority to approve expense reimbursements (authorization). Jimmy could create fake expense reports or inflate actual expenses. Since he has authorization power, he can approve these fraudulent expenses for reimbursement.

Jimmy then uses his custody role over the petty cash to withdraw the reimbursed amount. He essentially pays out the company’s money to himself based on the false or inflated expenses he approved.

Since this company wised up and hired an outside firm to do its accounting, Jimmy will probably get caught eventually. In the meantime, though, the fraudulent activities might go unnoticed. Similar scenarios could play out if a single person holds any other combination of two keys.

What if you are a small company, and segregating duties simply won’t work for you? The easiest duty to outsource to keep everyone honest is the recording duty. Your founders shouldn’t be spending time on accounting anyways, so this is money well spent. It also prevents fraud.

If authorization and custody are tough to split, open a giant window with transaction visibility access so that stakeholders can clearly see everything and keep people honest. People are less likely to commit fraud if they view their actions as open to the other executive team members.

Accounting Software

Now that your bank is set up and you properly segregated duties, you are ready to connect your accounting systems. But how to select a good accounting system? If you have a good accountant, they’ll simply guide you through the system selection process and get you onto the best system for your needs. If your accountant is passive and lazy like those described at the start of this chapter, you need to move on from this person and find someone who cares.

Suppose your company is still young and in the extreme scrappy phase where you have not yet hired someone to help with accounting. What should you look for in a good accounting system? The three factors that matter most are that your system should be cloud-based, should integrate with all your other systems, and should be a system that your accountant knows well.

Thankfully, cloud-based accounting systems are now the norm. Not too long ago, it was normal to have an on-premise desktop version of QuickBooks that only one person looked at regularly, who then sent a backup copy via USB drive to the CPA to do the tax return, who then made adjusting journal entries in a vacuum and sent the new version back to its box at the company to live until the following year.

Cloud-based systems are crucial if you want real-time data and real collaboration with your accounting team. This provides you with the option to give multiple users read-only access and have the business operations transparent to the leadership team.

Your accounting software also needs to integrate well with your other systems. Other systems include your payroll software, your customer payment collection system, banking, credit cards, and expense management systems. These integrations allow your accounting to become automated and more accurate.

Finally, you should choose accounting software that your chosen accountant knows well. Otherwise, they are going to spend too much time closing your books each month and errors become more prevalent.

At the time of writing, the two accounting systems that best check these three boxes are QuickBooks Online and Xero. Xero offers a more pleasant user experience, but QuickBooks Online integrates with many more systems. QuickBooks Online tends to be the optimal choice for most of our clients because these integration options are extremely valuable. More people are comfortable with QuickBooks Online operations as well. However, with time there is the possibility that Xero catches up with QuickBooks in terms of integrations and user familiarity.

Vendor Payment Systems

Making payments to vendors typically comes in three varieties—auto-payments, manual bank payments via check or direct transfer, and company credit cards. We will tackle best practices for each of these in turn.

Auto Payments

Regularly recurring expenses should be set to auto-pay every month, either by setting up an ACH bank connection or by inputting your credit card to automatically pay these bills on time each month. Examples include rent, utilities, fixed-fee contractors, software licenses, etc. You make the decision once to use the service if you are confident that you can pay for it moving forward, then simply execute on that decision automatically. If the service stops working for you, you cancel. What you don’t want to do is give yourself decision fatigue on which bills you’re going to pay each month.

You’ve already made the decision to use the item, so pay the rent, or electric bill, or whatever. No need to continue torturing yourself every month when you can use your decision stamina toward directing your company. I am constantly surprised at how many founders choose to manually write checks for items that stay relatively the same every single month. You have better ways to use your time, so spend your time on that instead. If something no longer works for you, then you cancel it.

Manual Bank Payments

How would you feel knowing your name, address, bank account number, and routing number traveled all over the place with nothing but an envelope to cover up that information? Once it gets delivered, you hope the right person opens that envelope with your sensitive information, but there is no way of knowing for sure.

The other issue with checks is that they can be stolen, washed, and cashed by the thief. This is one of the scams portrayed by Leonardo DiCaprio in “Catch Me if You Can”. Modern checks often have better security features, but this still poses a risk.

Thankfully, modern software has options for making vendor payments digitally. You will want to make sure your payment system offers a variety of user permission settings and layers of approval required to avoid the segregation of duties issues described in the banking section above.

Banks that offer digital payment often lack these features, so make sure to verify that cash is properly safeguarded. Vendor payment systems that our clients use include Bill.com, Melio, and Ramp. Intuit recently released a payment product as well, though we haven’t tested it yet. Which system you will need depends on your business and processes since each has its own flavor. For more guidance, check out our blog on 6 Practical Tips to Keep Your 501(c)(3) Organization IRS-Compliant in Montana.

You also want to set up your system in a way that seamlessly integrates with your accounting software. This improves speed and accuracy for managing these vendor payments.

Credit Cards

While it might be tempting to simply give every employee a company credit card, remember that access to a card gives the Custody key described above. Expenses can quickly get out of hand, and you don’t want to find yourself in a position where you have to babysit the company credit card account to make sure nobody is pushing the boundaries on what is allowable.

Ideally, your credit card system will seamlessly integrate with your accounting software (like all other systems) and have a process of approvals or limits set by team member. It is illegal for a rogue employee to go nuts with the company card and you can sue them for damages, but it’s much easier to simply limit access to begin with. Free company credit card systems exist because they get paid by the credit card company a portion of transaction fees generated. This is a win for you because you can get access to a great corporate credit card system at no cost.

You should be able to give your accountant view and record-keeping access to your credit card account to make the accounting seamless and streamlined. If your system does not allow tiered access and credit limits by card, find one that has the features you want.

Conclusion

Building a business in Montana—or anywhere—requires more than grit and vision. It takes structure, especially when it comes to your financial operations. Whether it’s choosing a bank with modern security features, segregating duties to prevent fraud, or selecting the right cloud-based accounting system, the right infrastructure empowers you to scale confidently.

Don’t settle for outdated practices or passive advisors. Set yourself up with systems that support transparency, efficiency, and long-term success—and let your accounting team do what they do best while you focus on leading the business forward.

Disclaimer: This article is for informational purposes only and is not intended as tax, legal, or financial advice. Always consult with a qualified professional about your specific situation. Reading this post does not create a CPA–client relationship.